The role of KYC in automated customer onboarding

Banks and financial institutions face a multi-faceted trade-off when it comes to the task of identifying customers in the consumer business in a manner that complies with the law. A limited – but growing – number of KYC (know your customer) procedures are available that meet the regulatory requirements for preventing money laundering. These are characterized by different advantages and disadvantages in factors such as cost efficiency, availability and usability. Given this background, how can compliance be simplified and processes made more automated and digital? We take a closer look at the options currently available for implementing KYC in the context of B2C banking products.

To begin with a disclaimer: BANCOS does not offer any KYC solutions of its own. As a long-standing developer of end-to-end onboarding processes for financial service providers, we would like to share our experience here on the integration of KYC solutions as vendor-independently as possible.

KYC as an elementary digital process module

When it comes to compliance and money laundering, the topic of KYC is mandatory for banks as part of their business relationships. However, in-person identification and the associated manual processes were still one of the main barriers on the way to automating onboarding processes long after the advent of digitization. Processes that had been common for a long time, such as PostIdent, quickly no longer met customer demands for convenient application processes that were as digitized as possible. In addition to the digitization of KYC, the connection with the qualified electronic signature (QES) plays a major role in automation. The combination of the two steps is what makes it possible to conclude a legally valid contract and, in the case of an installment or credit line application, to pay out the money to the (new) customer immediately.

How does a digital KYC process work today? Currently, the most common method for verifying identity is online identification via video chat (“video ID”). In this process, the applicant interacts with an employee of the solution provider, who performs various verification steps and interactions with the ID document and can thus help with any questions or problems the applicant may have. Providers of this KYC solution can usually link it to a QES, which allows complete digitization. This is a significant advantage of this KYC solution. The requirements for the applicant are also relatively low in times of more and more familiar video conferencing and high-quality smartphone cameras. The main disadvantage of video ID is its comparatively low level of automation. Due to the necessary personal interaction, it is not consistently available and manual steps by the verifier can lead to errors. From a compliance point of view, it should also be noted that video ID solutions from several providers were recently hacked by the Chaos Computer Club. As a result, it has already been banned as an identification method for the e-patient record.

Advanced development in the automation of KYC processes

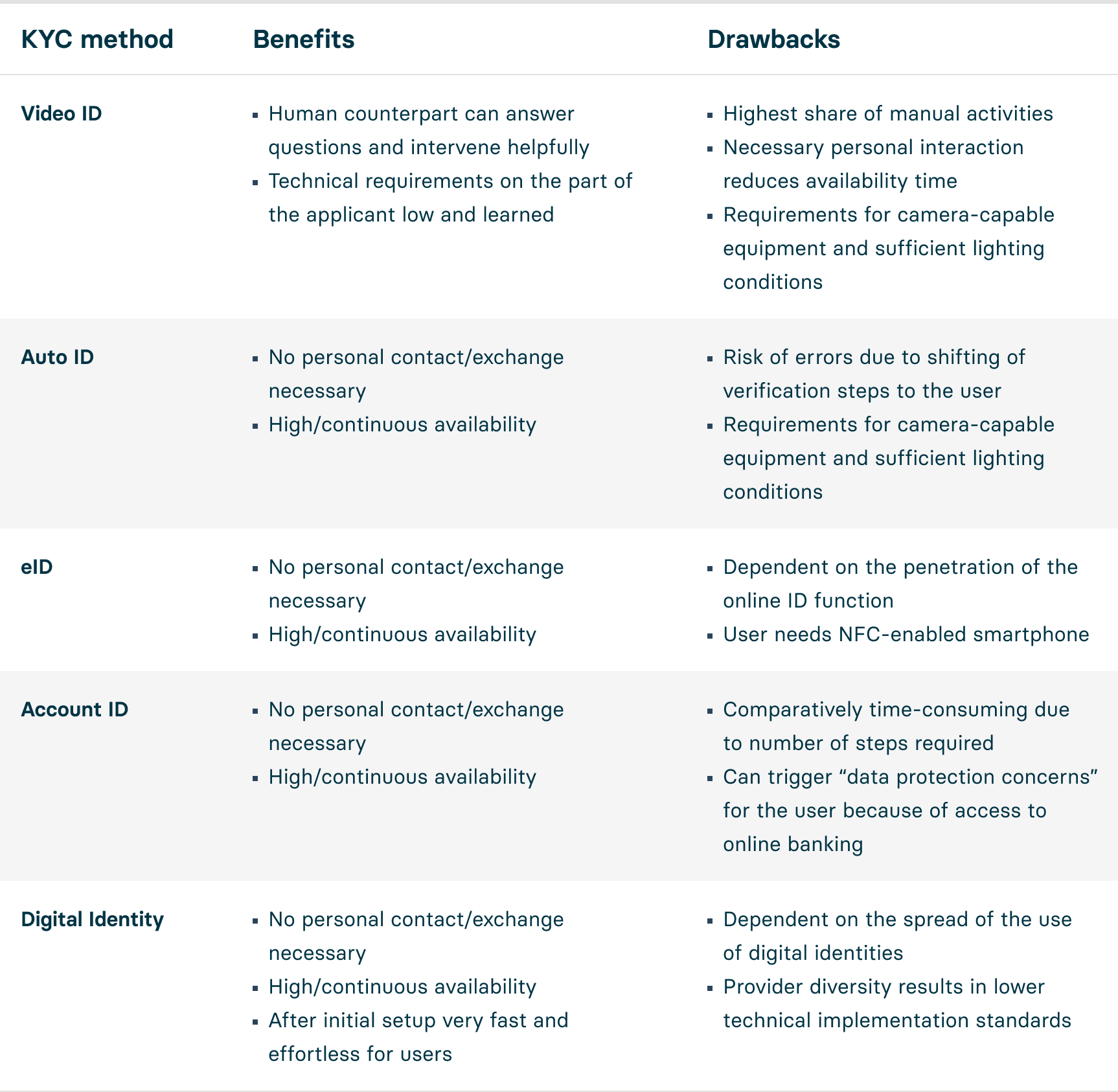

In addition to video ID, which dominates the banking sector, there are a number of other KYC processes available whose primary goal is further automation. What they have in common is that they bypass personal interaction with a verifying person. However, the implementation differs significantly in each case, which brings with it various advantages and disadvantages. The following table shows an overview of these for the KYC checks discussed here.

Auto ID: This solution uses biometric processes and is supported by artificial intelligence, according to providers. The customer first takes a photo of the ID document and is guided through an automated check of the security elements of the ID. A portrait photo or video is then taken and matched accordingly. The method enables very high availability compared to the “personnel-intensive” video ID. However, it also requires a camera-equipped device and sufficiently good lighting conditions.

eID: In this case, a German ID card with activated online ID function (eID) and a smartphone capable of NFC (near field communication) are required to verify identity. If these requirements are met, the customer reads out the ID data via an app, which already completes the process. In principle, this solution is convenient and secure. However, it should be borne in mind that the eID function is not yet very widespread in the German market and can therefore be a conversion barrier in onboarding as a sole option.

Account ID: The first step here is to take photos of the ID document and the applicant’s face. The face-to-face interaction for verification is then replaced by the customer’s login to online banking, where a one-cent transaction required by law is then carried out. Since the required identity checks can be performed via the bank account data, the process can be completed directly here as well. Due to the familiar actions for customers, the process is convenient. On the other hand, it can be disadvantageous for data-sensitive persons that they must share their online banking information with the KYC provider.

Digital identity: Services for a digital identity enable verified information and data to be stored centrally once. If these are required in an application process, they can be provided for verification via app/wallet without having to check them again each time. However, similar to eID, the use of digital identities is not yet widespread. In addition, there are a number of different providers, none of which has yet established a leading position in Germany, although potentially strong network effects can be assumed in this market segment. In addition, the diversity of providers is reflected in less developed implementation standards.

Which KYC process is best for my onboarding?

There is no one-size-fits-all answer to this question. In consideration of the technical development of the processes and the legal conformity required for their approval in terms of money laundering prevention, it is important for banks and financial service providers to continuously monitor the situation around KYC. The market and customer needs are moving further and further in the direction of speed and convenience – especially in the credit business – to which the alternative solutions offer advantages over the current standard video ID. However, these must be evaluated in terms of their potential disadvantages and barriers with regard to the respective customer target group.

In addition to an optimized customer experience, the costs of the KYC processes obviously play a decisive role in a final decision. As a guideline, it can be assumed that video ID as a digital solution has lower costs than PostIdent. However, in comparison with more automated solutions, the costs are usually higher due to the necessary personnel deployment.

A recommendable basis is a flexible technological infrastructure that enables the connection of the individually desired KYC solution through appropriate interface competence. One conceivable scenario could be, for example, to offer customers a choice of different identification methods in the application process, comparable to the decision for a payment option in e-commerce checkouts.

Our end-to-end solution BANCOS Onboarding for fully automated application processes includes such a flexible API architecture – for the KYC area, among many others. Find out more online here and feel free to contact us if you would like individual consulting or a personal demo.