How the credit decision shapes the digital customer experience

In addition to efficiency gains and scaling potential, automating processes in the lending business offers further benefits that have a strong impact on the customer experience at the point of sale. Automated credit decisions are particularly central to this – both in sales on credit comparison platforms and for the loan applicants themselves.

Sales platforms drive automation in credit decision-making

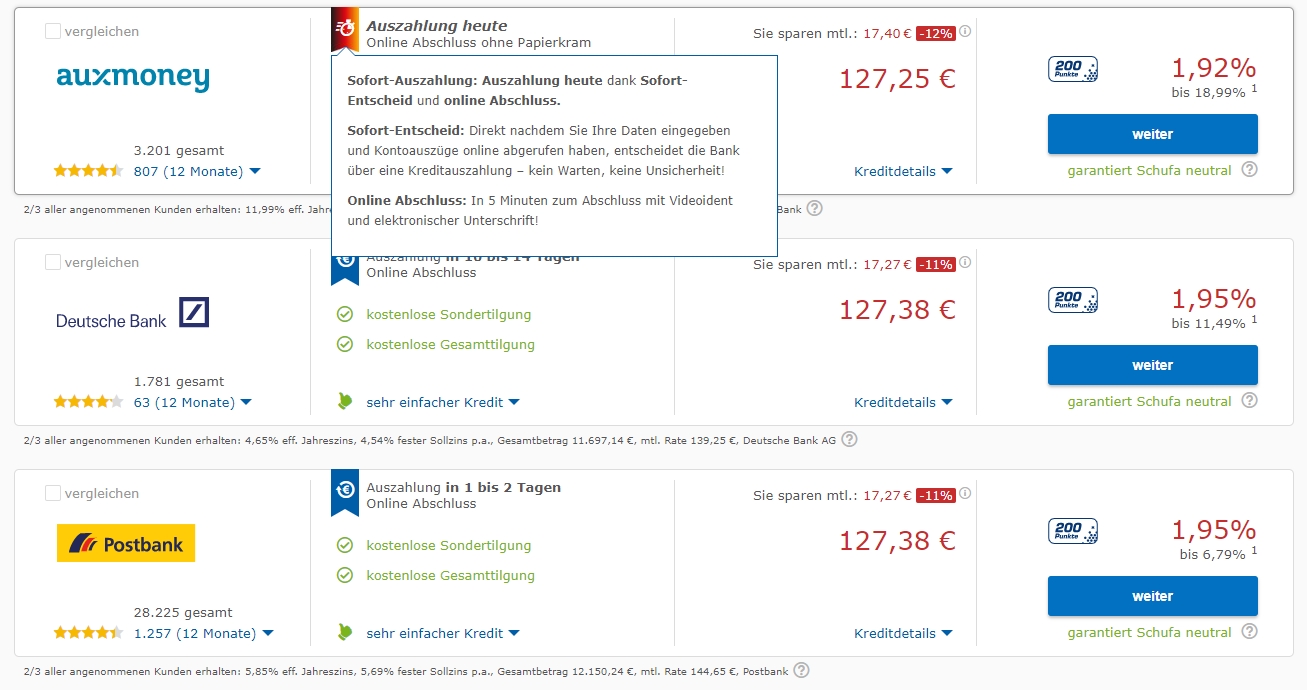

Especially in the area of standardized products such as traditional installment loans, platforms have long played a dominant role as a sales channel. Check24, probably the most important player in the German market, is worth a closer look. This is an example of how platforms are shaping competition not only at the sales level, but also at the digital level. Technical and procedural aspects of the individual loan providers are translated directly into information relevant to prospective customers at the point of sale. This approach becomes particularly clear around the credit decision and the associated time to disbursement of the loan. The following screenshot shows this as an example. Other platforms such as Verivox or Smava also design their credit comparison touchpoint in a similar way – albeit somewhat less prominently.

Excerpt results installment loan request on check24.de (18.08.2022)

This consistent highlighting of the time period until payout has a high priority for the platforms when interacting with customers. This is what Check24 founder Henrich Blase says about it in a podcast interview with the industry platform Finance Forward:

“The speed of the credit decision is the most important issue for us, besides the area of interest rates. Digitally affine customers in particular don’t want to receive any more paperwork after entering their data with us. Banks are still struggling in this regard now, but I think they will move tremendously in the next two to five years. That’s one of the top priorities for us in that area.”

Some banks and loan providers obviously already meet these requirements. On the other hand, when looking at the platforms, significant differences can still be observed in the time to loan disbursement. This is also underlined by figures from the study report “Credit Processes of the Future” by the management consultancy Horváth. According to these figures, the processing time for installment loans is still longer than 180 minutes at 23% of the institutions surveyed – a clear competitive disadvantage, especially on digital sales channels.

The customer experience as a differentiator in the lending business

Customers on the demand side of the market also have needs that speak for an accelerated and convenient credit decision. Last year’s “World Retail Banking Report” by Capgemini and Efma focused, among other things, on the topic of customer experience. On the one hand, it emphasized the importance of the “delivery” of a product that is difficult to differentiate at the product level, such as a loan, for the brand experience of a bank. On the other hand, the globally surveyed customers singled out the loan application process as the most complicated interaction (“highest level of friction”) with their bank. So there still seem to be gaps between the desired and the actual customer experience.

Another important development in customer behavior is also related to digital offerings and platforms that focus on convenience. Schufa’s current “Risk and Credit Compass” identifies a significant increase in small loans. These are mainly attributed to forms of “buy now, pay later” offers, the growing demand for which is particularly evident among younger age groups due to the low barriers to usage. Moreover, this development contributed to the fact that the number of installment loans taken out rose again in 2021 for the first time since 2017.

Full automation in credit decision-making as a solution

Banks therefore face a challenging situation between changing customer needs, powerful sales platforms with high technical demands, and the corresponding alignment of their own IT and software landscape.

A viable solution lies in the implementation of a comprehensively digitized loan application process. Central to this is the most complete automation possible of the credit decision, which can bring the competitive advantage on credit comparison platforms, among others. In addition to a transparent implementation of the parameters for the credit decision, such a solution must offer a flexible interface architecture to ensure a seamless process: from the inclusion of the applicant’s data on the platform, to the integration of service providers for credit checks, KYC and QES procedures, to the transfer of customer data to the existing core banking and CRM system.