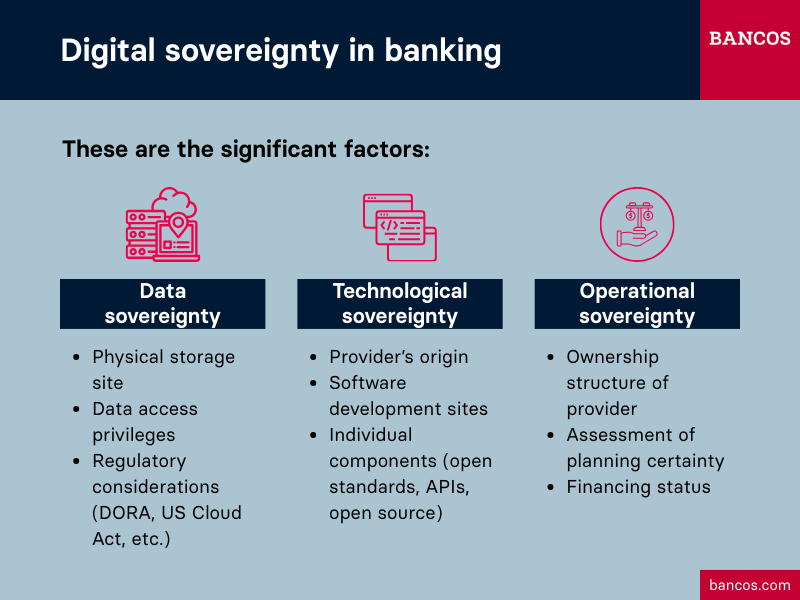

Data sovereignty: more than just the location of the data center

When talking about data sovereignty, they often think first of the physical location where data is stored. Data stored in a European data center is frequently considered secure and compliant. But this assumption falls short. What matters is not just where data is stored, but who can access it and under what legal framework.

How does international regulation affect digital sovereignty?

The U.S. CLOUD Act requires companies based in the United States to hand over data upon request by U.S. authorities—regardless of whether that data is stored in the U.S., Europe, or elsewhere. For European banks that use cloud services or software solutions from U.S. providers, this creates a structural conflict with the GDPR and other European data protection regulations.

Since January 2025, the DORA Regulation has further tightened the requirements for third-party risk management in the financial sector. Banks must document which third-party providers they use, where their infrastructure is operated, and the legal framework governing data processing. In addition, the EU Data Act has been fully applicable since September 2025, introducing, among other things, rules for switching between cloud providers and aiming to reduce vendor lock-in.

True data sovereignty requires a combination of technical, contractual, and organizational measures. A sovereign cloud is characterized not only by the location of the data centers but also by the ability to migrate data and applications as needed and to ensure that no unauthorized external access occurs.

Technological sovereignty: the type and origin of the tech stack matter

In addition to data-related issues, another question is coming into focus: Where do the technologies themselves come from? The risks of relying solely on non-European technology providers are manifold. They range from price increases and changes to licensing models to the denial or delay of security updates, and even politically motivated access restrictions. These risks can significantly limit freedom of action: If a provider acts restrictively when it comes to licenses or access, banks face a choice between acceptance or a costly migration.

What technological aspects strengthen digital sovereignty?

European software providers can offer an alternative here. It is crucial that the technology is not only hosted in Europe but also developed and refined there. This directly addresses the European legal framework and industry-specific requirements.

In the area of core banking systems, it is also advisable to examine the individual technological components. Proprietary interfaces, vendor-specific cloud platforms, and closed architectures exacerbate dependency effects—not only at the commercial level but also across the entire technology stack. Open standards, API-based architectures, and the use of open-source components, on the other hand, promote technological sovereignty. They enable the replacement of individual components without jeopardizing the overall system and reduce dependence on a single provider.

Operational Sovereignty: ownership structure as a strategic factor

One aspect that is often overlooked when assessing digital sovereignty concerns the ownership structure of the technology providers themselves. Whoever owns a software company determines its long-term strategic direction, investment priorities, and pricing policy. For banks that rely on a single provider’s solutions for their core processes, this issue is anything but abstract.

How do software providers’ ownership structures affect the degree of sovereignty?

In recent years, the European financial IT landscape has seen increasing consolidation. Private equity firms or large international players, often based outside Europe, are acquiring local software providers. What may bring capital and economies of scale in the short term harbors risks in the medium term: changed product strategies, the relocation of development capacities, rising license costs, or the discontinuation of product lines that do not fit into the portfolio.

For banks seeking long-term planning security and a reliable technology partner, the independence of the ownership structure is therefore a relevant selection criterion. A provider with a stable, independent, and ideally European ownership structure offers greater assurance that strategic decisions will be made in line with the interests of customers and the European market. During due diligence for potential providers, questions such as the following should therefore be addressed: Who owns the provider? How stable can these ownership structures be considered? What is the financial situation?

Key Takeaways for Digital Sovereignty in the Banking Sector

- Growing awareness: one of the top technology trends for financial service providers

- A process, not a condition: gradual improvement as an appropriate goal

- Synergy of measures: implementing data sovereignty technically, regulatorily, and organizationally

- “Looking under the hood”: examining individual components and development processes of software solutions for technological sovereignty

- Know the technology partners’ stakeholders: identifying ownership structures and deriving their implications

BANCOS, an independent European software provider based in Berlin, has been developing core banking and automation solutions for banks and fintech companies since 1988. Learn more online here and contact us if you would like a personalized consultation.